By John Capuano, Co-Founder of Simplicity Lone Beacon,

and Marcus Roth, Senior Director of Data Automation, Email, and Content

Consumer attitudes toward money and investing are more relevant than ever to the world of financial planning. We’ve mined and analyzed these trends for nearly 15 years, and our most recent study sheds light on the things that are most critical to U.S. investors who are near or in retirement. The 2025 study gathered insights from nearly 2,000 people who are in or approaching retirement.

We surveyed Gen-Xers and Baby Boomers from all corners of America and found that they have more similarities than differences in financial concerns and preferences.

The Data

We surveyed a nationwide database of individuals across a demographic, geographic, and qualitative spectrum during the first quarter of 2025. The outreach aimed to uncover how people are feeling about retirement and what shapes their financial decisions. We compiled the data of about 2,000 people that we believe best represent the American investor.

Total Participants: 1,696

Age Range

- 69% were between the ages of 61 and 74

- 31% were between the ages of 45 and 60

Net Investable Assets (excluding real estate):

- 4% reported having $3 million (m) or more

- 22% fell into the $1m to $3m range

- 27% had between $500,000 (500k) and $1m

- 27% reported between $250k and $500k

- 19% had less than $250k

Principles of Retirement Planning: What People Said

One of the foundational sections of our survey asked participants to rate key elements of retirement planning—Longevity, Liquidity, Inflation, Market Risk, Legacy Planning, and Tax Mitigation.” Respondents were asked to rate the importance of each element on a scale from 1-5, 5 being extremely important.

Longevity: Not Running Out of Money

This was by far the top concern. A full 77% of respondents rated longevity planning as extremely important. This sentiment was universal across all wealth tiers, proving that no matter how much someone has, the fear of running out of money in retirement is real.

Liquidity

While most participants rated liquidity as moderately important, those with $500,000 or less in investable assets were 20% more likely than average to say liquidity was “very” or “extremely” important. For people in this range, maintaining flexibility and cash flow is likely a pressing day-to-day concern.

Inflation

Worries about inflation remain top of mind. Most respondents across wealth segments rated inflation protection as either “very” or “extremely” important, signaling a general anxiety around purchasing power and the rising cost of living.

Market Risk

Roughly 70% of respondents rated market risk as “very” or “extremely” important, with the level of concern consistent across all wealth tiers. Volatility is a universal concern, and this tells us that clients are looking for ways to feel more secure in unpredictable markets.

Legacy Planning / Mortality

Interestingly, legacy planning scored right in the middle for most people. The most common score was a 3 out of 5, indicating that while some thought it was essential, a good portion hadn’t made it a top priority. This suggests an area of opportunity for more education and planning conversations.

Tax Mitigation

This topic received widespread importance across the board. However, high-net-worth individuals (especially those with $3m+) were 20% more likely to rate tax mitigation as “extremely” important. This may suggest that as wealth grows, so does the perceived benefit of sophisticated tax strategy.

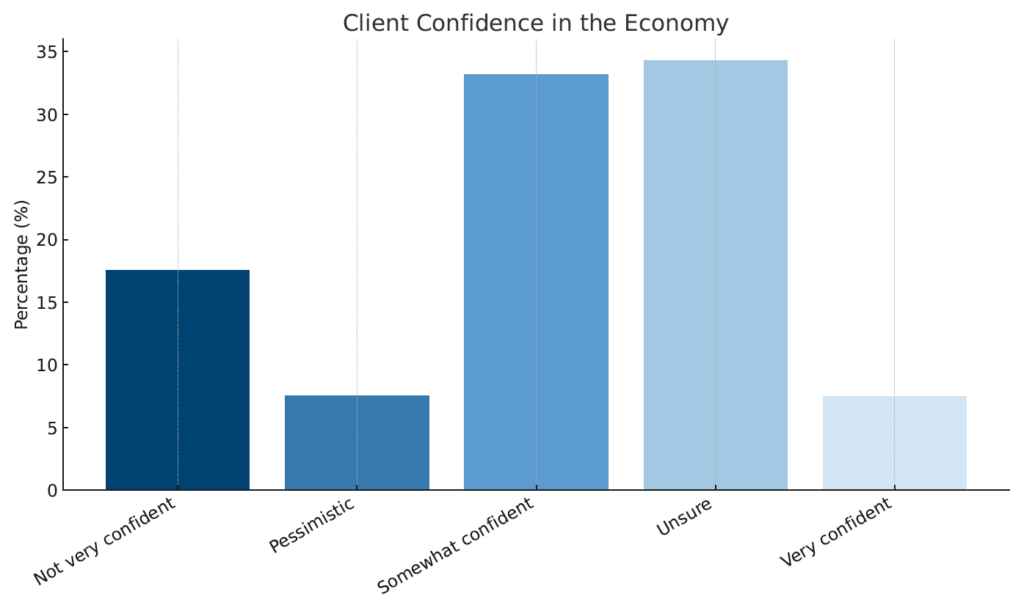

Confidence in the Economy

When asked how they feel about the economy:

- 35% said they are unsure

- 33% were somewhat confident

- 17% said they were not very confident

- 8% felt very confident

- 8% were pessimistic

This means 92% of respondents fall somewhere between “pessimistic” and only “somewhat confident”. In fact, nearly 60% are unsure or expect worse.

Trust and ease have always been big motivators to get people to act in times of uncertainty, potentially now more than ever.

The Role of a Full-Service Financial Advisory

When asked how important it is to have all their financial needs serviced by one source:

- 44% said it is somewhat important

- 42% said it is very important

- 15% said it is not important

That means nearly 90% of respondents see at least some value in a consolidated, full-service experience. The even distribution between “somewhat” and “very” suggests that many may not fully understand what this kind of support can offer—perhaps seeing it as a luxury, rather than a value-add.

Interestingly, those who had $3m+ in net investable assets had increased responses of “not very important”. This may suggest that those with more wealth are interested in specialists in certain strategies or are interested in having multiple advisors with different strategies and products.

Retirement Risk: How Much Are People Willing to Risk?

The question of risk tolerance revealed clear trends:

- 57% would risk a small amount for reasonable growth

- 25% would risk 20–30% of their savings for a higher return

- 18% would not risk anything at all

Higher-net-worth respondents were slightly more willing to be risky. Among those with $1m or less, 22% said they wouldn’t risk anything. Compare that to just 12% in the $1m–3m bracket, and only 7% of those with $3m or more.

Risk can be a very relative variable. Everyone is wired differently, plus market conditions, and our world is constantly changing. It may be a good idea to recalibrate the definition of risk on an individual level.

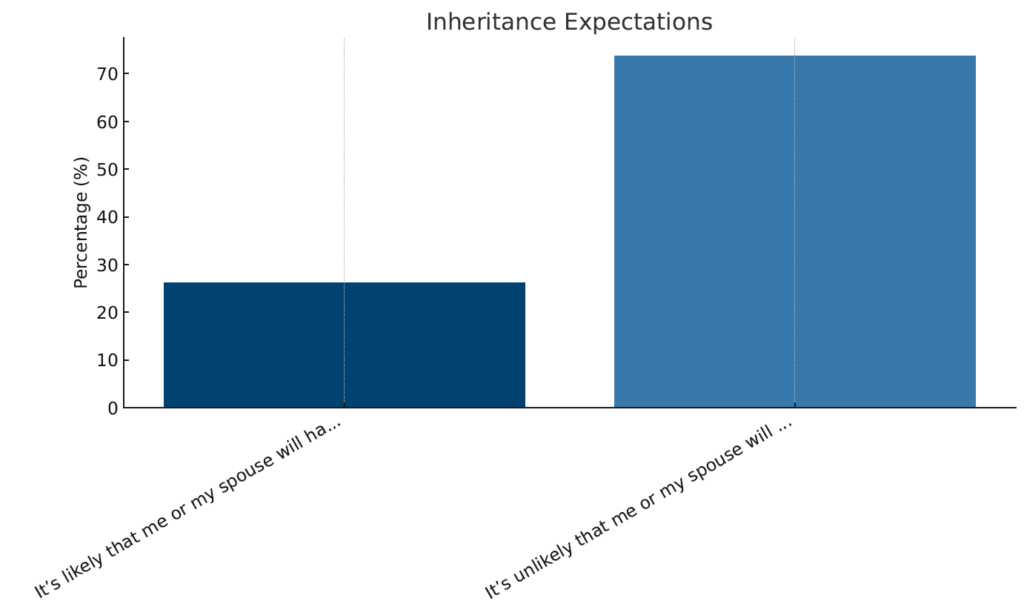

Inheritance Expectations

We asked whether respondents believed they would receive an inheritance:

- 26% said yes

- 74% said no

This differed significantly by age:

- Among those aged 45-60, 50.4% expect to receive an inheritance

- Among those 61-74, only 24.5% believed they would

Wealth transfer continues to be one of the largest opportunities in our industry. Estimated at $104 trillion by 2034. The conversations about wealth transfer should take on a different tenor between Gen-Xers and Baby Boomers as Gen-Xers are twice as likely to expect an inheritance.

Financial Media Habits

How often do people engage with personal finance topics in the media?

- 29% said weekly

- 18% said daily

- The rest only a few times per year

That means nearly 50% of people scroll through finance content at least weekly.

Therefore, to have a competitive advantage, advisors must become their trusted source for financial topics, particularly when prospects are lower in the sales funnel. As we’ve observed, short-form, authentic video content is the hottest trend in marketing.

Long-Term Care Readiness

Responses varied:

- 36% feel confident in their care plan

- 32% are unsure

- 24% are concerned

- 8% said they would rely on family

Those with $1m or more are twice as likely to feel confident in their plan compared to those with $500k or less. People with $500k–1m are average, and this could be an ideal group to engage with education and support.

According to a recent study, 80% of long-term-care policies sold are generated via the client asking their advisor. This continues to be a big opportunity in the financial industry.

Physical Health in Retirement

When asked about wellness in retirement:

- 51% said it’s already important, and will continue to be

- 35% said they plan to focus on it more

- 14% said they would rather relax

This pattern held across all wealth tiers, showing broad concern about health. Maybe it’s time to think beyond steak dinners at local upscale restaurants. What about “Finance & Fitness” workshops?

One great example of how health and finance intersect comes from Harvard Pilgrim Health in Massachusetts, which offered a free pair of workout sneakers to seniors who signed up for new health insurance policies. It’s a small gesture with a big message: you’re buying from a company that knows personal wellness is a priority.

What People Value Most

We asked respondents to rank lifestyle interests. The following is the percentage of answers that ranked this category as “extremely important”.

- Health and Wellness (55%)

- Family and Social Connections (48%)

- Travel and Leisure (37%)

Meanwhile, continuing education and philanthropy/charity ranked much lower, indicating they are less of a focus in this phase of life. These priorities were consistent across all wealth levels.

Conclusion

Perhaps the most interesting finding, and the one that continues to have been the most consistent over nearly 15 years of such studies, is that people’s attitudes are largely similar. While answers and trends may evolve, they evolve in a “herd mentality” and remain uniform across geographic, demographic, and socio-economic lines.

It reminds us that humans have far more in common than we might think. We know that consumers are alike, and we know that financial professionals are alike in the strategies and tools they use to help their clients. So, this suggests that the most effective differentiation an advisor may offer is their understanding and personal connection with the individuals they work with. Since most people who work with advisors are the same from a surface level view, and a lot of advisors are the same from that surface level view, what will make you stand out as an advisor is your personal connection with the people who come into your office. Understanding what’s most important, establishing understanding, empathy, and trust will become the currency that separates the firms that will capture the most market share for the next decade.

About the Author: John grew up in Schenectady, NY & received a scholarship to Norwich Academy. He began his broadcast management career at WOR, learning spoken word marketing from the best in the business with a specialty in financial and long-form. John managed broadcast sales for some of the best-known sports teams in the world, at the most legendary stations. However, his true passion is in the world of direct response advertising to baby boomers and their parents. In this space, he has worked with some of the best brands in America. John lives in Boston with his wife, Melissa–a fellow broadcast executive–and French Bulldogs Lou and Sal.

About the Author: Marcus Roth is Simplicity Lone Beacon’s Senior Director of Email, Data, Automation & Content. Marcus has unique experience in B2B and B2C start-up companies ranging from enterprise-level market research of Artificial Intelligence to self-defense eCommerce products. His experience in AI market research brought him, and his research, to INTERPOL, The United Nations, and Harvard University.